I am slightly cutting with tradition here and skipping the analysis and jumping straight to the conclusion. I will add stats and analysis later along with my Social CRM Customer orientated Engagement Framework (i may need to come up with a shorter name). I will base this upon what i have learnt in this experiment and with an eye to enabling other customers out there to learn from my mistakes and engage companies through social media successfully. This will be added to the blog in installments during the upcoming weeks.

IF Vahinkovakuutus Customer Service Conclusions

One of the goals of this experiment was of course to get customer service via social media and Facebook in particular. I will start by summarising my thoughts with regard to this.

How did this score as a customer service experience in terms of technology?

Well in terms of my own experience of having to wait for responses it is no different than any other chanel a company may have you operate in. You write your question and wait for your response so in this respect it is the same as email, phone, web portal or even face to face conversation. This is as almost always the response is, "we will get back to you". This means that actually the experience is not so much affected by the technology but more by the company in questions own practices. However for me personally, it is a more than acceptable form of communication and fits with my own online presence. It is convenient and more so than having to remember passwords or logging in securely to a dedicated service which in itself causes added pain. Not really a good place for passing secure documents but a nice place to have the conversation.

How did the experience score in terms of the service i received from If Vahinkovakuutus?

As i will discuss this in terms of SCRM in the next section i will just approach this in terms of general customer service.

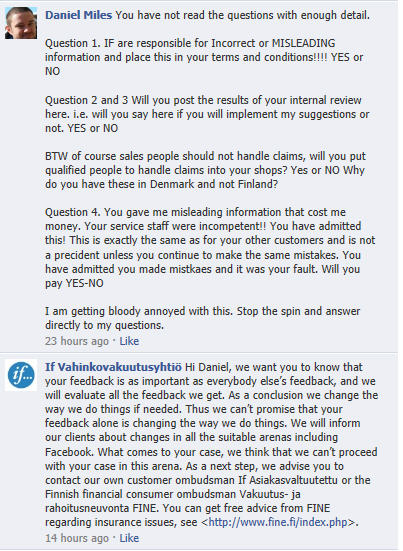

With If vahinkovakuutus's responses i was annoyed in the delay in responses to my questions. Particularly where at one point they disengaged for two days and then still did not answer my questions. This made me feel like they were just ignoring my concerns and they were just hoping i would go away. This gave me the impression that they were childish. I was not attacking them i was not slandering them i was attempting to engage them in dialogue and discussion with what i felt was a valid argument.

I was also frustrated by If vahinkovakuutus's almost constant effort to get me off Facebook and force me back into their conventional channels. If vahinkovakuutus seem to only want to use Facebook as a marketing channel. They do not really want to engage me as a customer and they certainly do not want anything that could be perceived negatively there. What they do not understand they themselves can affect this perception by their own behaviour and how they react to the content that is placed there.

I was particularly disappointed that If Vahinkovakuutus did not want to publish results publically with regard their review into using a third party for their emergency customer service or for their lack of customer service in their shops. This just made me feel like they were not actually going to do anything and their promise to investigate this was just PR. I believe that they were not listening at all and i am left with the feeling that nothing will happen. I always felt like If vahinkovakutus had something to hide.

I was also very disapointed that, even though If admitted that they made mistakes, they still refused to compensate me for the costs that their miscommunication had caused me. This is something i just cannot get my head around to be honest. Basically the message i received is too bad we do not care!

Also the they refuse to even discuss any changes to their terms and conditions. I requested that they should, accept liability in the case if incorrect or misleading information supplied by them. This just makes me feel sorry for their other customers.

Finally, two weeks ago i asked for a copy of the phone call that If based their decision not to pay on, this has still not reached me. This suggests to me that they have something to hide or are afraid that i will publish it. This gives me the impression that If vahinkovakuutus are not a morale company and you cannot trust them.

Social CRM Conclusions

The main goal in this experiment was to engage a company through their own social media and to see, if by doing so, the customer has gained more power in the conversation than through conventional channels.

In this respect i think that although my own personal goals of changing If vahinkkovakuutus's behaviour for the benefit of their other customers and gaining compensation for myself were not succesful i believe the experiment has been. This is why.

Having engaged If vahinkovakuutus through their own private channels i was unsuccesful in achieving my personal goals. I was not going to get my money back anyway, so in this respect nothing ventured nothing gained applies. All that this has cost me is my time.

More importantly by engaging If vahinkovakuutus in this public space i brought awareness to my cause. By gaining support i was able to apply pressure to If vahinkovakuutus above that that i could have through their own channels. From this factor alone the probability of success must rise even with the real danger of annoying them. This is because all of the advantages are the customers. The cusotmer has nothing to lose That is as long as they do not alienate their audience.

This strategy also has the power to benefit the company through excellent customer service (as so often has been demonstrated) and has added value as a marketing tool. However the strategy also allows for the company to be embarassed publically and to devalue their own brand and disrupt their messaging. This has additional potency of course as the conversation is held on the company's own social media and infront of their own stakeholders. This is the worst case scenario for the company and involves the largest risk and cost for them. This of course depends upon how the company themselves behave and the ingenuity of the customer. Unfortunately for If vahinkovakuutus i feel that they fall firmly into the second category.

If vahinkovakuutus have embarassed themselves and eroded their brand equity. This is why.

If' vahinkovakuutus's poor performance is not only about the poor customer service experience that i received (as discussed above) but also from their own attitude towards the use of social media. At all turns they attempted to get me off their Facebook group. They did not want to engage me there.

For some time, the fact that they tried to ignore me and hoped i would go away, is also a very immature attitude to this kind of dialogue. However in this situation i was able to diversify my strategy on their facebook page and other social media to interfere with their own marketing messaging. I believe that, this was the only reason that after two days they did re-engage me. In the social media world there is nowhere for them to hide and in this way the customer is empowered when they act in a civilised way. Again this must always be in a dialogue and never slanderous or you will lose your support and alienate your own audience. It is hard to do sometimes but, it essential to avoid losing your temper. You must always consider how you are perceived as an individual.

If vahinkovakuutus were aware of the risks of blocking me on the Finnish Facebook group. I had forseen that this may happen and had a backup plan but did not have to use it. I was however temporarily blocked from the other If Insurance local social media Facebook pages. I do not know where this decision came from but it says something about If's corporate culture with regard social media. Rights however were returned when i noticed and blogged about it. This again indicates a degree of empowerment. In terms of appearing as a caring socially responsible company this is of course totally unacceptable behaviour. The content that i added was of course not explicit or offensive to any of If's audience.

If vahinkovakuutus clearly only see social media as a way of pushing out their own message and they wish to control it at all cost. They even asked me not to post content related to my blog.

Sorry no you cannot control social media.

Facebook is a public forum, you may start the conversation but you should not try to control it. If vahinkovakuutus seem not at all interested in engaging customers in dialogue especially things that relate to their poor performance or things that are painful for them. Actually i believe this is a Finnish trait generally. This type of engagement is of course one of the mantras of Social CRM. I wonder if If vahinkovakuutus had ever heard of social CRM before this experience. One thing is for sure, they have now.

Additional benefit gained from engaging If vahinkovakuutus in the social media world is also in terms of the company's own costs related to the claim. By prolonging this claim i increased If's own financial costs for this claim dramatically and in all likelihood substantially more than the value of the original claim. This is another factor that empowers the customer. In traditional channels it is easy to diengage a customer when you have had enough of them. In the social media world it "looks bad" so it is harder for a company to do so. This means that as a customer you can continue to force the company to incur additional cost in handling your grievances and increase the pressure on them.

What was the ROI for If vahinkovakuutus?

How have If vahinkovakuutus come out of this experience? Financially the actual costs for handling the claim must be way above what they would have been had they just paid the claim in the beginning. They have also had a lot of negative publicity targeted at their own stakeholders and a permanent reminder of their poor performance preserved in this blog for all time and thanks to my SEO efforts this should be visible to people who search for If Vahinkovakuutus for the foreseeable future.

On top of this i can see from the stats that about 30 people visiting the site clicked an insurance related advertisement. Statistically and based upon the source of my traffic at least half of these were If customers or stakeholders as they came from If's own Facebook pages. I would love to know if even one of these customers switched from IF to a competitor as a result of this. This is a cost to If i cannot measure and only guess at.

Furthermore as half half of my traffic came from the UK and US and none of these are If countries this is probably the first that those people have ever heard of If vahinkovakuutus. As such this is the first impression that will affect their image of If vahinkovakuutus as a brand. You know what they say about first impressions. This becomes even more pertanent if If vahinkovakuutus decide to venture into those markets.

Really it beggars belief that a company could be this stubborn, childish and damn stupid. As a manager i would have settled in the beginning taken the opportunity and sold the marketing story. I would have eliminated all risk from this. Especially as the customers case is a valid one and the original value of the claim was only 500 euros. I thought insurance companies were big on assessing risk and ROI.

Well it just shows me that even in the face of a valid argument (by their own admission) they will not put their customers first even when it is in their interest to do so. I just cannot understand this, it makes no sense at all.

What was my own ROI for this Experiment?

Well personally i did not do well, i was unable to turn over the claim decision and admittedly i spent a lot of time on this. However i have learned alot about how to engage a company and i can share that with others and i will. This blog is an enduring testament to that.

In the upcoming weeks i will add new content here that will outline a

Social CRM engagement model/framework from the customers perspective. The purpose of which is to show customers how to succesfully engage a company in dialogue pertaining in particular to Social CRM. I will also add more content related to analysis of channels and statistics. In this way customer's everywhere will be able to learn from my mistakes and successes to engage with their own service and product providers.

Perhaps then the ROI for me is in terms of legacy. I hope that others can learn from this experience and apply some of the techniques. I also hope that companies themselves will learn from this and learn how to and how not to engage customers. At least everyone (including me) should learn something about

Social Customer Relationship Management.

Conclusion

During this process i tried to find other examples of someone trying this kind of engagement and was unable to do so. All of the literature seems to have been written from the company's perspective in terms of their marketing successes. As far as i know this is the first time a customer has deliberately attempted to engage a company in an organised dialogue and not a rant and as part of a wider self organised social media campaign. Of this i can be proud.

As a final note, i managed to gain 50% of my traffic through If vahinkovakuutus's own social media. This meant i was able to target their own audience, on my site, with insurance advertisements from If's competitors. Originally this was to increase the pain to If vahinkovakuutus. Although the revenues are small from this endeavour (a few cents so far) and profitiability was not the point of this experiment, in about 100 years i should have recouped the losses originally caused to me by If vahinkovakuutus. In this respect on a long enough time scale this endeavour will not have cost me anything. This means the only costs were incurred solely by If vahinkovakuutus.

Well done If, we salute you! Sometimes when you win you lose and sometimes when you lose you win. Given a long enough time scale of course.